By Anna Gray at BWCI

anna.gray@bwcigroup.com

“a range of sanctions, including in the most serious cases,

substantial fines and imprisonment for criminal offences.”

This is a summary only. Legal advice should be sought to understand the position in relation to any specific circumstances.

The new duties on employers to auto-enrol staff into a pension scheme are set out in our basic guide to secondary pensions. However, it is not always appreciated that, for those with existing pension schemes, this is not simply about checking that the contributions satisfy the minimum requirements.

Changes are likely to be needed around how and when employees are enrolled into a pension scheme, as well as some other more technical aspects. Not complying with the new requirements can lead to enforcement action. The Guernsey Revenue Service (GRS) has a suite of powers it can use. This note looks at some of the potential consequences.

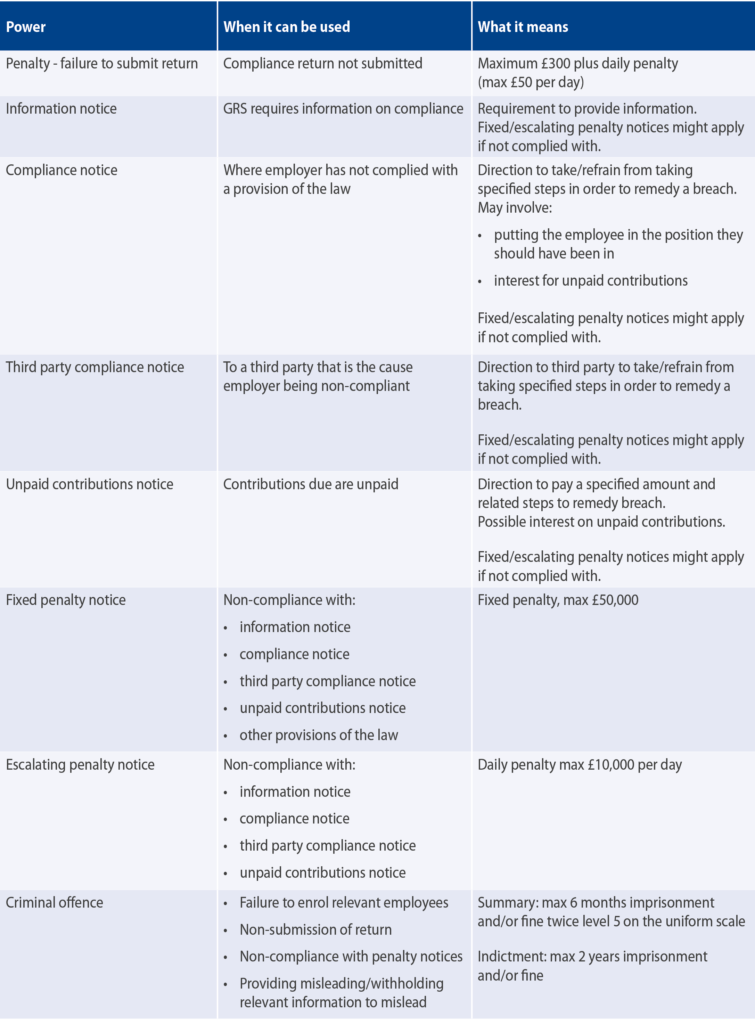

- New GRS powers allow it to:

- obtain information,

- direct steps to achieve compliance/prevent recurrence of non-compliance,

- require payment of unpaid contributions (plus interest), and,

- impose a fixed fine (max £50,000) and escalating daily fines (max £10,000 per day) to ensure compliance.

- Additionally, non-compliance with the enrolment duties or penalty notices can be a criminal offence leading to imprisonment, a fine or both.

- It is also an offence to provide false or misleading information or for employers to omit relevant information.

The consequences are not just relevant to employers:

- Third parties causing the employer to be non-compliant can receive a “third party compliance notice”.

- Where an employer is a legal person, partnership or unincorporated body, directors or equivalent officers might be subject to enforcement (for non-compliance with enrolment duties and non-payment of penalties) if the non-compliance was carried out with the officer’s consent, connivance or neglect.

- Information notices may be sent to employers, but also employees or pension scheme administrators.

Time will tell how often the GRS will need to use its powers, but the very similar regime in the UK has led to a number of high profile fines and prosecutions.

It is important that employers understand how the new requirements will affect them so that they can prepare well in advance. BWCI can assist in providing a pension scheme that meets the new requirements.

Summary of enforcement powers